1-800-548-4639

1-800-548-4639

You’ve finally escaped the inescapable — your tax debt. Lifting this burden from your shoulders can be a massive relief, but it can also leave you on edge about what to do after paying off debt. After pouring extensive time and resources into combating debt, you might not know what steps to take next. Maybe you have lingering worries about accumulating debt again, and are looking for ways to avoid that. Or, perhaps you’re unsure where to start redistributing your new budget.

Whether you’re solely focusing on avoiding debt or wondering how to put your energy toward earning and saving, there are solutions available to you. Everyone’s tax debt is different, depending on the cause, your assets and various other factors. Below are some of the paths you can take to maximize your post-debt lifestyle and eliminate the possibility of falling into debt again.

Lower Your Yearly Tax Rates

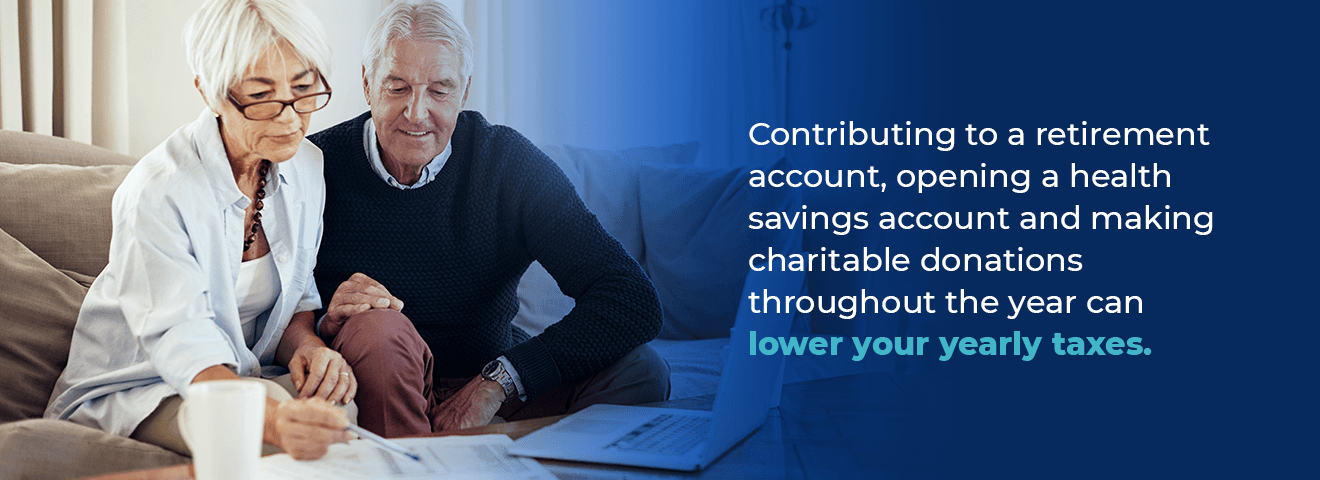

Once debt is off the table, you might feel like you’re still holding your breath and waiting for the accumulation to start all over again. However, you can take several steps to lower your tax liability altogether, creating less room for tax debt to creep up. Contributing to a retirement account, opening a health savings account and making charitable donations throughout the year can lower your yearly taxes.

For these actions, you’ll most likely need to itemize your returns rather than opt for the standard deduction. This process will take more work, but will be well worth it in the end. One of the first things you can do to adjust your tax return amount is to reassess your W-4 form. Since this tells employers how much to withhold from your paycheck, changing your W-4 can make a considerable difference in how much you owe or get back in April.

Contributions you make to your retirement account get deducted from your taxable income, and therefore reduce the amount of tax you’ll owe based on income. If your employer doesn’t offer a 401(k) or similar plan, you can always consider an IRA instead, which takes contributions from pre-tax dollars. Even if you have a 401(k) plan, an IRA account is still an excellent booster option. There are limits to how much you can contribute to IRA accounts based on retirement plans offered through your work, but Roth IRAs and traditional IRAs are options to look into. Also, if you currently hold stocks, you can use them as a form of charitable giving. Many nonprofit organizations accept stock transfers that count equally toward your annual philanthropic deductions.

For self-employed people, special deductions and tax credits may be available to you. For instance, if you provide health insurance to your employees, you might take advantage of the small business health care credit. Some tax deductions are different for self-employed people, such as a home office, continuing education, phone and internet costs and more. Also, there are several retirement plans for side businesses.

The foremost thing to remember about reducing your tax liability is document, document, document. Without an accurate record of your charitable donations or other choices that can lower your taxes, the IRA will not accept these. Start detailing each financial decision for liability reasons with the IRS and to become more aware of your investments.

Budget, Save and Invest

Now is the perfect time to reassess your budget. Most likely, you were putting a substantial portion of your extra money toward debt payoff for a while. With this off your plate, you have the freedom to redirect your spending to various investments. While you’ll want to save most of it, set aside a small amount of your money to use toward extra goods — whether it’s clothing, dining, home renovation or anything else, it’s well-deserved after spending so much time dealing with debt.

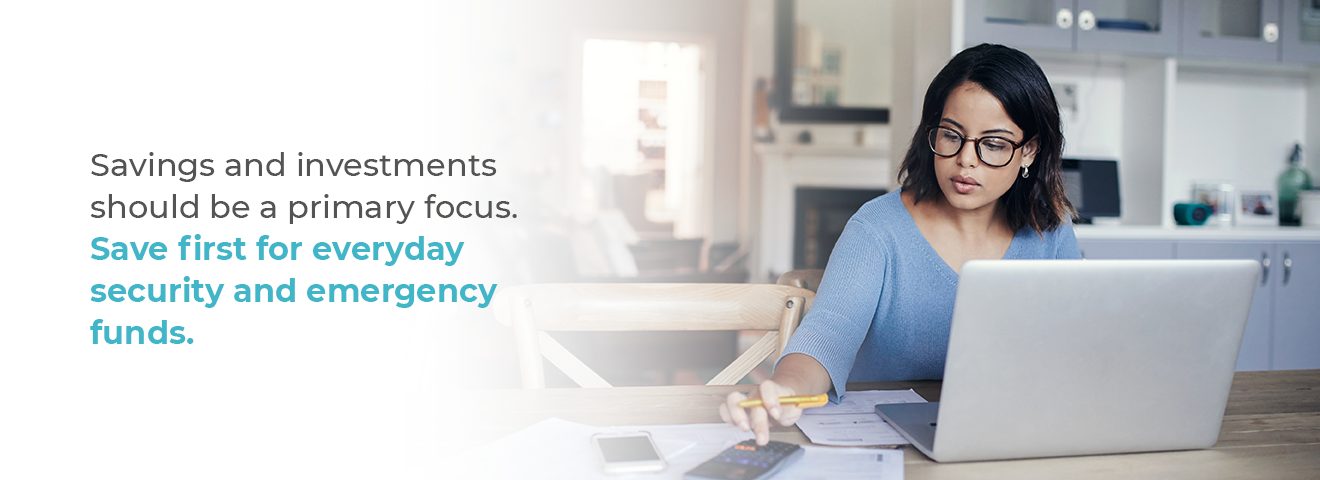

Savings and investments should be a primary focus. Save first for everyday security and emergency funds. Having a comfortable margin to work with for rent, phone bills, groceries and other regular bills can feel like a heavy burden has lifted and allows you to breathe if any life events arise that result in unexpected expenses. Once you feel satisfied with the amount you have put aside for that, focus on saving for specific items. Now is an excellent time to put extra funds toward your car, mortgage or a vacation.

Investing is an option that many Americans are turning toward for saving and earning. By putting your money into the stock market or redirecting part of your paycheck toward a 401(k), you are automatically setting aside money that will benefit you in the long run and eliminate the temptation to spend it on other things. The choices for investing are vast, ranging from stocks to rental properties to cryptocurrency. Plus, the appeal of this for many is that you don’t need to set aside a large amount of money to start the process.

The stock market is the most common way for people to start investing. Fundamentally, the stock market allows you to put money toward something in the hopes that it will gain additional profit over time. Moving around your funds is an individual choice, and other than that, you mostly have to check in on the stocks’ performance periodically. Plus, many brokerage organizations will consider the level of risk you are willing to take with your investments, making investing approachable even for inexperienced people. If you don’t know where to start, hiring a financial adviser and learning about investment jargon is a great foundation. Finding the right investment option for you takes some time and research, but can be rewarding in the long run.

Perhaps rather than putting money away for a rainy day with investing, you already have a loftier goal in mind. Use this time with newfound financial flexibility to start saving for your future. Create a fund for traveling to a bucket-list destination, earning a degree, moving or anything else that would add value to your life. Planning and budgeting for this goal can be a rewarding way to take advantage of your nonexistent debt and make your life more enjoyable.

How to Prevent Tax Debt

After paying off your tax debt, one of your essential focus areas is avoiding future debt. Taxes can be a significant stressor, especially if you’ve had a negative experience with them in the past. In addition to lowering your taxes and adjusting your budget, making minor changes to become attentive to taxes year-round can make a world of difference.

One of the most surefire ways to avoid back taxes is having a reliable system for filing taxes each year. Ensuring you have everything in order long before April 15 is crucial to staying organized and on top of potential debt. Track what tax credits and deductions are available for you and keep detailed records of your yearly expenses with receipts or handwritten notes. Maintaining a record of your financial moves will save you from playing catch-up and feeling overwhelmed when April rolls around.

If you owe more than you can pay at the moment, the IRS may allow you to pay by using a credit card or even paying the balance over an extended period. Submitting Form 4868 to the IRS will provide an automatic extension that gives you through Oct. 15 to perfect your tax return if you owe individual taxes. While it’s best to file your taxes early, this option can prevent you from going down a slippery slope. The late filing penalty is 5% of the tax owed per month, up to a maximum of 25% of the balance, if you fail to file your tax returns or Form 4868. However, remember that you must disclose what you believe you owe when submitting the form. If you fail to turn in this form by the tax filing deadline, the IRS will charge the late filing penalty, late payment penalty and interest.

Once the IRS grants you an extension, always thoroughly examine your tax return yourself and use a fresh set of eyes to look things over. Talking to a tax professional or using a trustworthy tax software application can help you catch things you may have missed. Using this six-month extension allows you to finalize your finances and squash any uncertainty about your taxes turning to debt.

Looking at tax prevention as a sequential, step-by-step process will make it less overwhelming. Back taxes can snowball, as they take effect even if partially paid and accumulate interest and penalties. If you find yourself in a situation where you cannot avoid the snowball effect due to unforeseen life events and changes, remember that tax forgiveness is available. If you know how much you owe, you can work with the IRS to fulfill payments partially, or with the Offer in Compromise plan.

If you feel yourself slipping into accumulating back taxes, don’t feel like you have to tackle it all on your own. Reach out to a tax consultant — they can review past tax returns, ensure you have filed them correctly, suggest additional tax debt forgiveness strategies and even help you negotiate with the IRS to limit the amount of interest and additional fees you’ll have to deal with.

Tax Preparation and Planning

Above all else, avoid debt and back taxes with a system that works for you. Pay attention to the area of spending or avoidance that got you into debt in the first place, and reassess your steps for handling that item. For example, if credit card debt was the issue, stop using the card. Use alternative payment methods like debit cards or cash that take out money in real time.

Educating yourself and building confidence about your tax bracket and what you owe is a great way to plan for tax season. Know the difference between tax deductions and credits and understand how itemizing deductions works. Pulling yourself out of debt can be a long process, but there are resources available to ensure your taxes remain manageable in the future.

It’s a best practice to keep a record of your annual tax returns. Knowing how much you paid or got back and what documentation you used will keep you organized and prepared if the IRS ever decides to audit you. Usually, the IRS has three years to decide whether to conduct an audit, but it’s never a bad idea to hang onto older returns just in case.

Tax planning allows you to avoid debt and have some extra money in your pockets, but it’s also ideal for addressing tax concerns or issues, saving for retirement and preserving funds for your heirs. Federal income tax planning is a vital part of ensuring your taxes are manageable. Once you have this mastered, you can use the same methods for retirement, estate and small business tax planning to maximize your financial stability.

How BC Tax Can Help You Remain Debt-Free

The feeling of relief that comes with being debt-free is unlike any other. Not only are you independent from needing to keep up with consistent payments, but you can also start to redesign your budget and focus on debt prevention. If you aren’t sure where to start, or want the security of knowing you have industry experts by your side, BC Tax can help with our tax planning and preparation services. Put the stress of dealing with the IRS on us and contact our office for a free consultation. We can help you strategically navigate your debt-free life with planning and preparation services in Colorado and nationwide.

Authored by the BC Tax Insights Team, this article reflects the collective expertise and experience of our seasoned tax professionals. The Insights Team at BC Tax comprises specialists with a deep understanding of various tax scenarios and solutions. With a focus on providing informative, accurate, and practical insights, our goal is to guide readers through the complexities of taxation and financial planning. Every piece is crafted with the intent to help individuals and businesses navigate the ever-evolving world of taxes, ensuring clarity and confidence in decision-making.